I think you can perform Predictor Importance test and see which are the variable explaining the most.

There is this package named Boruta, you can go through the link for implementation in python.

You can eliminate the variables which are highly correlated. For example if you have age as the target variable and you have DOB as a feature then it makes no sense to build a model. So, you need to make sure to eliminate the variable which are highly correlated to the target variable.

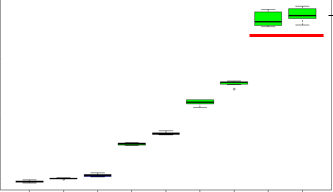

In my Scenario I had this following visualization

As you can see the 2 variables(underlined with red dash) are highly correlated with the target variable, before removing these variables the MAE was 0.9(approx) after removing those features(Backward Stepwise Elimination) and the MAE was 3.5(approx) but that is the actual error. Currently working on getting some external features to explain the data and to improve the accuracy. Every time it is not about accuracy/error rate of the model, it is also about how good our model could be generalized and robust our model should be.

To check if the data is overfitting, then I tried testing it by taking those 2 variables and try modelling and the MAE was 1.6(approx) from this we can understand that these 2 variables explain the most.

So, try applying and see how the features are correlated with the target variable.

One of the methods used to address over-fitting in decision tree is called pruning which is done after the initial training is complete. In pruning, you trim off the branches of the tree, i.e., remove the decision nodes starting from the leaf node such that the overall accuracy is not disturbed. This is done by segregating the actual training set into two sets: training data set, D and validation data set, V. Prepare the decision tree using the segregated training data set, D. Then continue trimming the tree accordingly to optimize the accuracy of the validation data set, V.

You can go thorough this link, about how we can avoid over fitting by tuning the parameters.