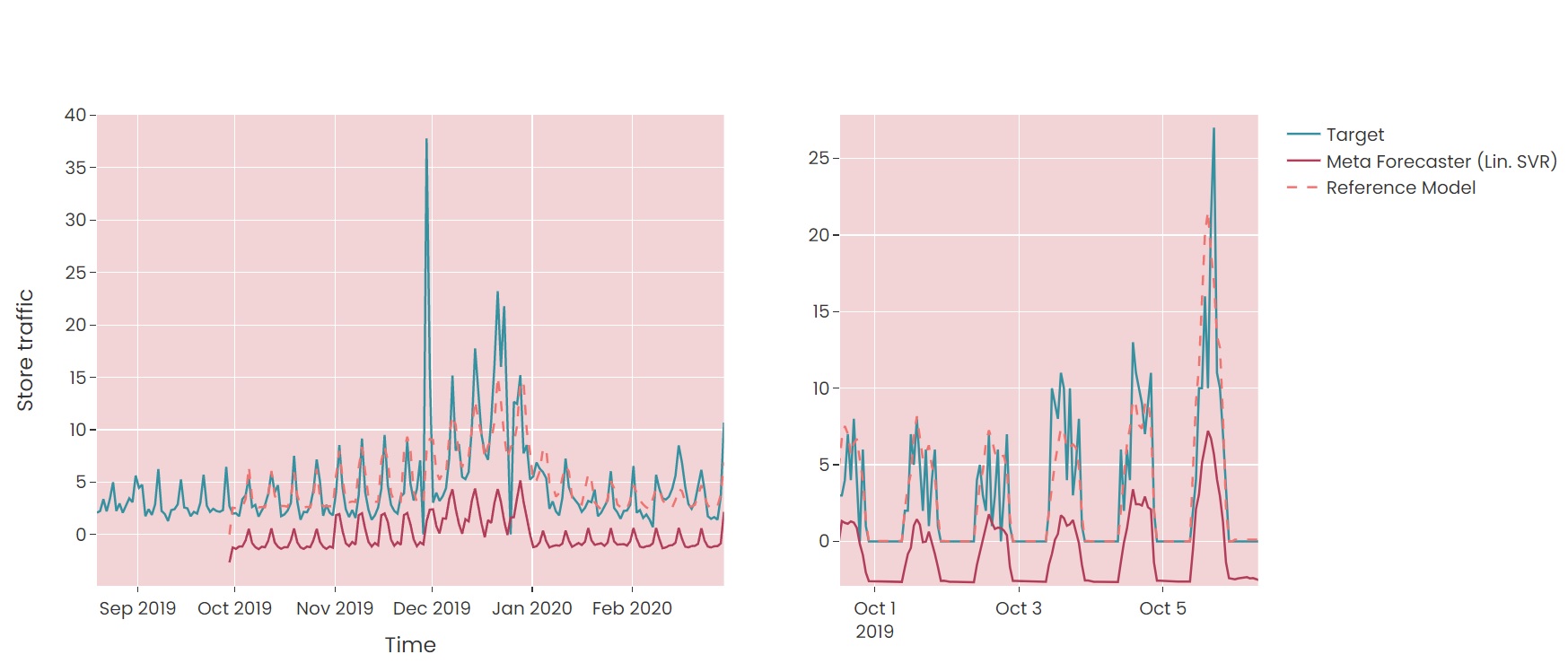

I have built nine meta models based on the model stacking principle, which I compare to a reference model for a number of time series. See the results below. The 22 base models that are trained on 70% of the training data produce forecasts on the last 30% of the training data on which the meta models are trained. These are then validated on the test set (last 20% of all data).

The Lin. SVR model's hyperparameters are set as follows, with other hyperparams. set to their default values:

C=0.1, fit_intercept=False, loss='squared_epsilon_insensitive', dual=False

Interestingly, the Lin. SVR models perform very poorly, which is an exception to the other models. Looking at their forecasts, we see a strong, consistent negative bias. If we ignore this bias, the forecasts are not that bad. What would explain this behaviour, and how could it be remedied?