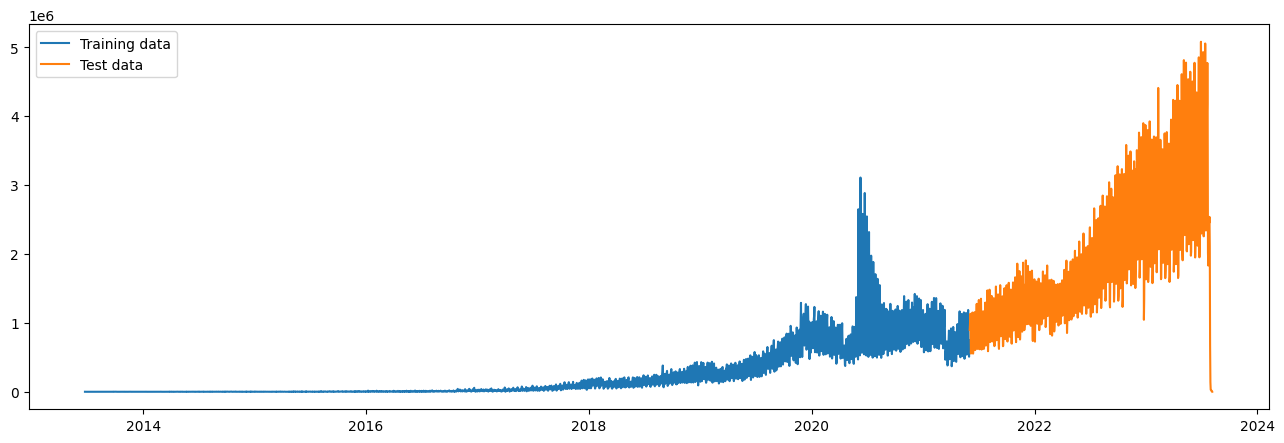

I have a non-stationary time series where I am trying to build a model for forecasting. So far on test set it produces multiple cycles no matter which technique I use.

There's just one feature Transaction Amount and index of the dataframe is datetime. Data spans past ten years. Around 3500 samples. You can see the data here:

I made the data stationary using diff, dropped the NaN and then I created additional features this way:

def create_features(df):

df['date'] = df.index

df['hour'] = df['date'].dt.hour

df['dayofweek'] = df['date'].dt.dayofweek

df['quarter'] = df['date'].dt.quarter

df['month'] = df['date'].dt.month

df['year'] = df['date'].dt.year

df['dayofyear'] = df['date'].dt.dayofyear

df['dayofmonth'] = df['date'].dt.day

df['weekofyear'] = df['date'].dt.isocalendar().week

X = df[['hour','dayofweek','quarter','month','year',

'dayofyear','dayofmonth','weekofyear']]

y = df["TRANSACTIONAMOUNT"]

return X,y

I used this to separate test and train datasets' y component:

X_train, y_train = create_features(train)

X_test, y_test = create_features(test)

Then I used XGBOOST with different parameters as well as MapieTimeSeriesRegressor.

reg = xgb.XGBRegressor(n_estimators=1000,early_stopping_rounds=50)

reg.fit(X_train, y_train,

eval_set=[(X_train, y_train), (X_test, y_test)],

verbose=True)

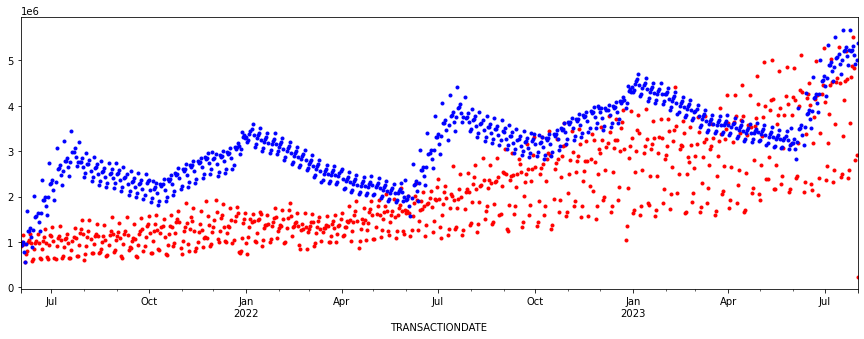

produced (after converting back to original using cumsum):

With XGBOOST having hyperparameters tuned:

With XGBOOST having hyperparameters tuned:

best_params = {'subsample': 0.6, 'reg_lambda': 0.05, 'reg_alpha': 20, 'n_estimators': 1000, 'min_child_weight': 5, 'max_depth': 10, 'learning_rate': 0.15, 'colsample_bytree': 1.0, 'colsample_bynode': 0.7, 'colsample_bylevel': 0.9}

reg = xgb.XGBRegressor(early_stopping_rounds=50,**best_params)

reg.fit(X_train, y_train,

eval_set=[(X_train, y_train), (X_test, y_test)],

verbose=True)

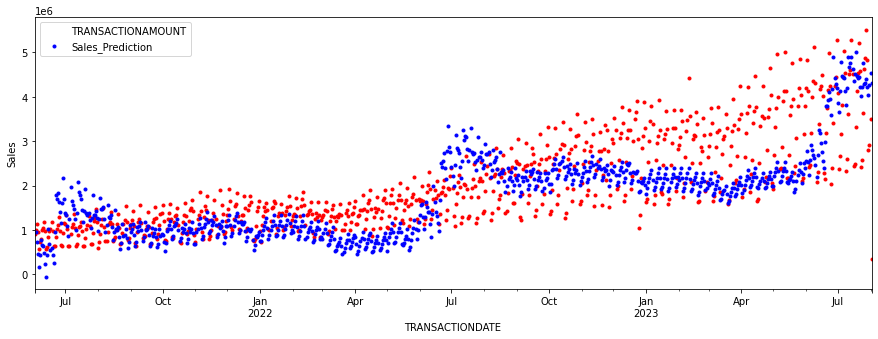

produced:

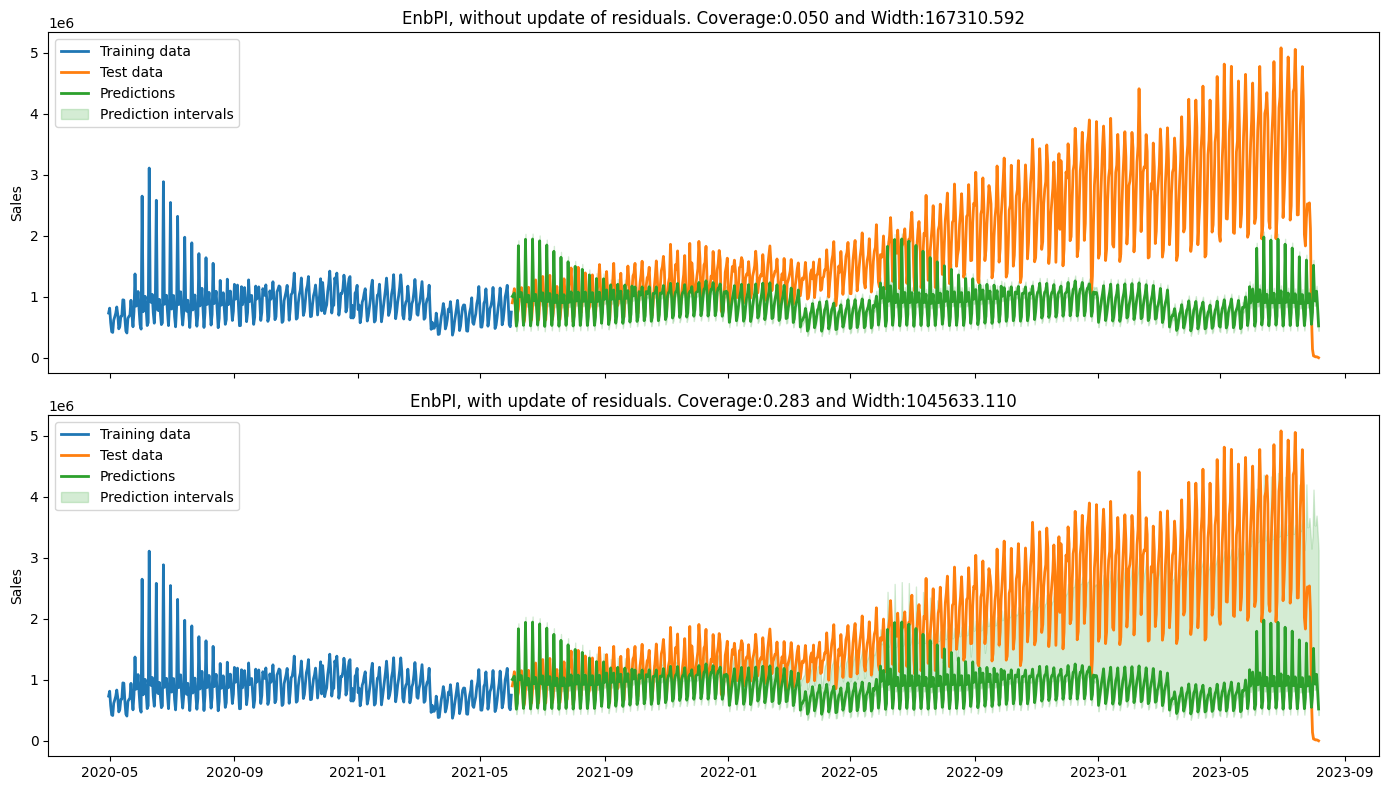

and finally, Mapie with and without update of residuals (taken from their tutorial on website):

and finally, Mapie with and without update of residuals (taken from their tutorial on website):

You can see at least three cycles in every prediction set. These are basically copies of the training set repeated multiple times. How do I get rid of them and make a better prediction?

You can see at least three cycles in every prediction set. These are basically copies of the training set repeated multiple times. How do I get rid of them and make a better prediction?