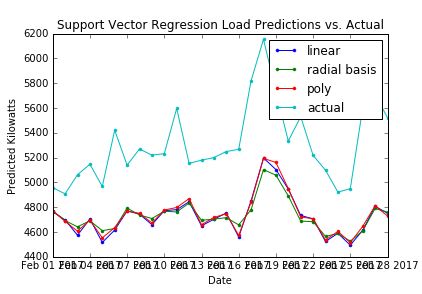

I am running an SVR prediction on some time series data, and I am receiving this weird offset between my actual and predicted values.

I found this SVM Regression lag post, that mentions adding a lag of 2 data points behind, instead of one. However, I am not sure how to incorporate that into my code (which I've included below).

Does anyone have any ideas on why my predicted vs. actual is offset in this manner?

My code is as follows:

#! /usr/bin/python

import math

import statistics

import visualizer

import numpy as np

from datagen import constructData

from sklearn import svm

# Applies Support Vector Regression to the electricity dataset,

# prints out the accuracy rate to the terminal and plots

# predictions against actual values

def suppVectorRegress():

kernelList = ["linear","rbf",polyKernel]

names = ["linear","radial basis","poly"]

preds = []

# Retrieve time series data & apply preprocessing

data = constructData()

cutoff = len(data)-30

xTrain = data[0][0:cutoff]

yTrain = data[1][0:cutoff]

xTest = data[0][cutoff:]

yTest = data[1][cutoff:]

# Fill in missing values denoted by zeroes as an average of

# both neighbors

statistics.estimateMissing(xTrain,0.0)

statistics.estimateMissing(xTest,0.0)

# Logarithmically scale the data

xTrain = [[math.log(y) for y in x] for x in xTrain]

xTest = [[math.log(y) for y in x] for x in xTest]

yTrain = [math.log(x) for x in yTrain]

# Detrend the time series

indices = np.arange(len(data[1]))

trainIndices = indices[0:cutoff]

testIndices = indices[cutoff:]

detrended,slope,intercept = statistics.detrend(trainIndices,yTrain)

yTrain = detrended

for gen in range(len(kernelList)):

# Use SVR to predict test observations based upon training observations

pred = svrPredictions(xTrain,yTrain,xTest,kernelList[gen])

# Add the trend back into the predictions

trendedPred = statistics.reapplyTrend(testIndices,pred,slope,intercept)

# Reverse the normalization

trendedPred = [np.exp(x) for x in trendedPred]

# Compute the NRMSE

err = statistics.normRmse(yTest,trendedPred)

print ("The Normalized Root-Mean Square Error is " + str(err) + " using kernel " + names[gen] + "...")

preds.append(trendedPred)

names.append("actual")

preds.append(yTest)

# Change the parameters 2017,2,1 based on the month you want to predict.

visualizer.comparisonPlot(2017,2,1,preds,names,plotName="Support Vector Regression Load Predictions vs. Actual",

yAxisName="Predicted Kilowatts")

# Construct a support vector machine and get predictions

# for the test set

# Returns a 1-d vector of predictions

def svrPredictions(xTrain,yTrain,xTest,k):

clf = svm.SVR(C=2.0,kernel=k)

clf.fit(xTrain,yTrain)

return clf.predict(xTest)

# A scale invariant kernel (note only conditionally semi-definite)

def polyKernel(x,y):

return (np.dot(x,y.T)+1.0)**0.95

if __name__=="__main__":

suppVectorRegress()