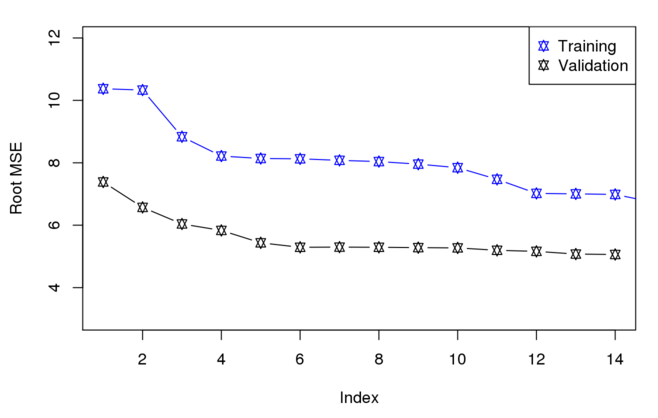

I’ve a model with 14 dependent variables (all of them are significant) and 678 observations. I used best subset regression and validation set (33% of data for the validation) to find which statistical model has the lowest MSE (for my curiosity). I got the following graph which surprisingly the MSE for validation data set is always lower than training data set for all the models (from 1 to 14 dependent variables). Here is the code that I used,

library(MASS)

set.seed(1)

train=sample(seq(678),452,replace=FALSE)

train

regfit.exh=regsubsets(HPV~. -Model.Types..code.-Year..code.,data=Mydata, nvmax=NULL,force.in = NULL, force.out = NULL, method="exhaustive")

val.errors=rep(NA,14)

x.test=model.matrix(HPV~.-Model.Types..code.-Year..code.,data=Mydata[-train,])

for(i in 1:14){

coefi=coef(regfit.exh,id=i)

pred=x.test[,names(coefi)]%*%coefi

val.errors[i]=mean((Mydata$HPV[-train]-pred)^2)

}

plot(sqrt(val.errors),ylab="Root MSE",ylim=c(3,12), pch=11, type="b")

points(sqrt(regfit.exh$rss[-1]/452),col="blue",pch=11,type="b")

legend("topright",legend=c("Training","Validation"),col=c("blue","black"),pch=11)

How come the validation root MSE could always beat the training?. Any feedback would be appreciated.

{kind=link}